The New Normal

As spring nears the end of the runway, dealers continue to report solid retail trends, with some caveats. In speaking with our dealers and reviewing data from dealer management system (DMS) providers and statistical agencies, new and used sales look very similar to 2023. Many dealers reported solid in-dealership foot traffic last month while they spoke candidly about some of their challenges. Increasing costs, adverse interest rate terms and growing inventory levels top the list of many dealers’ concerns. In addition, data suggests longer dealership sales cycles and significant margin compression on both new and used sales versus last year. While the light of spring is quickly fading, April price trends at auction were right in line with our expectations.

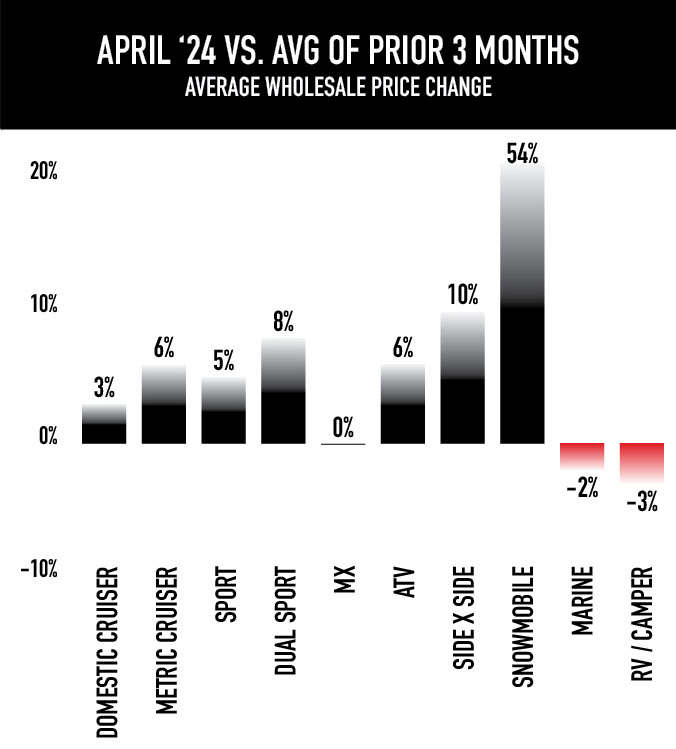

Riders Still Moving the Market

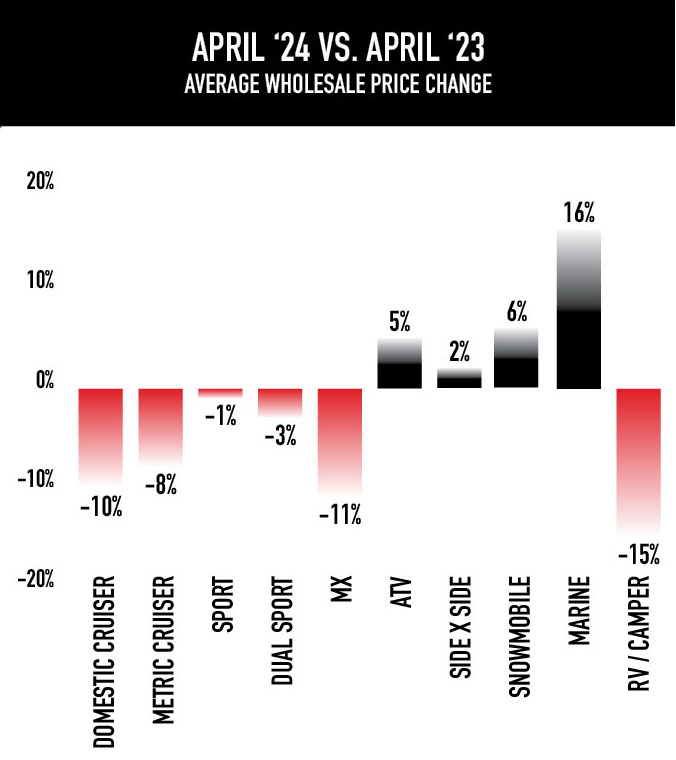

In April, overall average wholesale price (AWP) in the lanes continued to be solid versus the short-term comparable. “Core” powersports segments (domestic cruiser, metric cruiser, sport, motocross, dual-sport, ATV and side-by-side) all performed equal to or better than the prior 90 days. While we experienced a slower ramp in the first 60 days of 2023, AWP increases kicked into gear in March and continued to show strength in April. When looking back year-over-year, the performance is more mixed but very much aligned with expectations given the continued realignment with pre-COVID trends. March saw declines across the board versus 2023, but April AWP trends were flatter when comparing year-over-year performance. While most other segments have seen normal variations, sport-bike values continue to command a premium in the marketplace.

The Backside of the ‘Peak’

As we look into May, it’s important to note that AWP historically dips from the March/April peak. In normal years (2018, 2019), it’s not uncommon to see May pricing come in 5% to 7% lower than prior months. While we expect early May AWP trends to be strong, dealers typically begin to downshift their buying habits as the spring selling season transitions into summer. As we’ve been highlighting for well over six months, contending with increased levels of inventory will be the biggest challenge our industry faces this year. Continued promotional activity and rate subvention on new product will help move units in the short term, although it could have a massive impact on used value trends and dealership profitability in the back half of this year. The good news is that May will be better than June or July, which means there is still time to reach out to the team at NPA for more information and guidance. Proactive inventory management will be key to dealer profitability.