Summer Has Begun

As we officially leave spring and move quickly into summer, average wholesale prices (AWP) continue to follow our forecasted trends. May values show strength versus 2019 comparables while trending below last year’s pricing. AWP trends generally follow season norms but at levels that suggest additional softening in the market should be expected. Dealer management system (DMS) data exhibited solid trends in new unit sales through the first four months of the year while continuing to display a buildup of unsold inventory at dealerships. With new inventory levels significantly above that of 2019, expect OEM promotional activity to continue to increase through summer and fall, influencing buyer bid behavior in the lanes.

It’s Time to Act

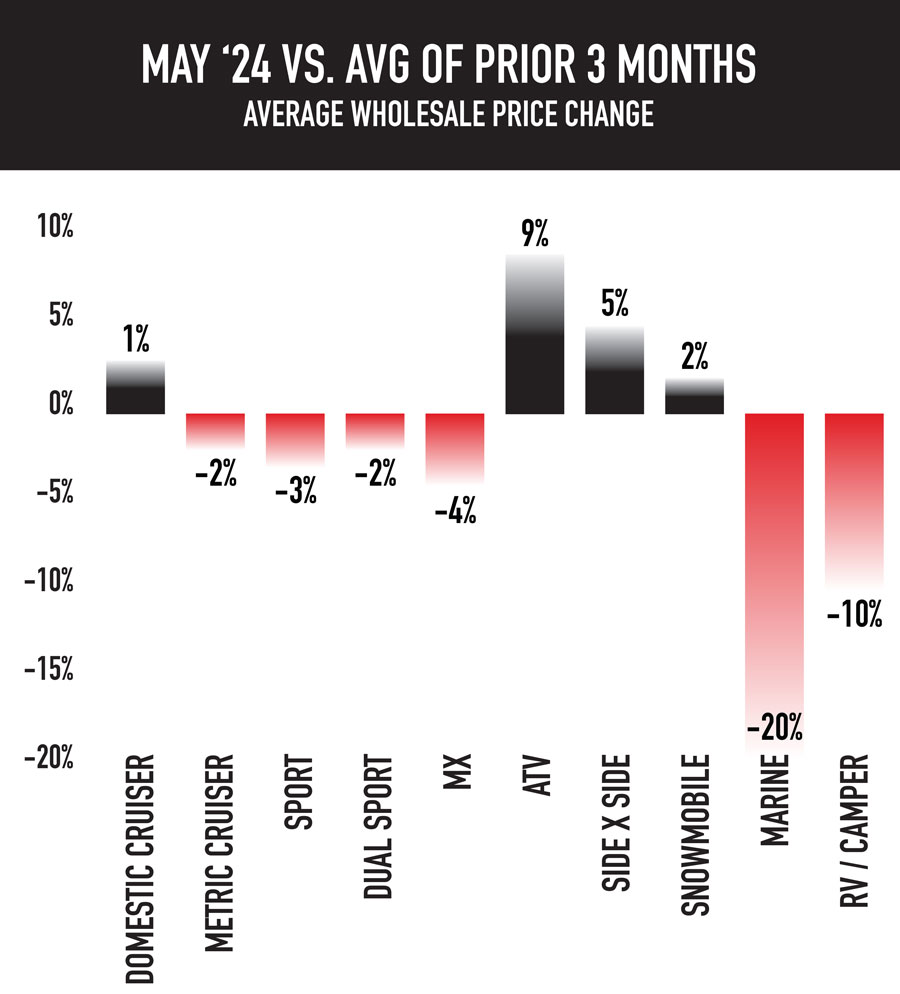

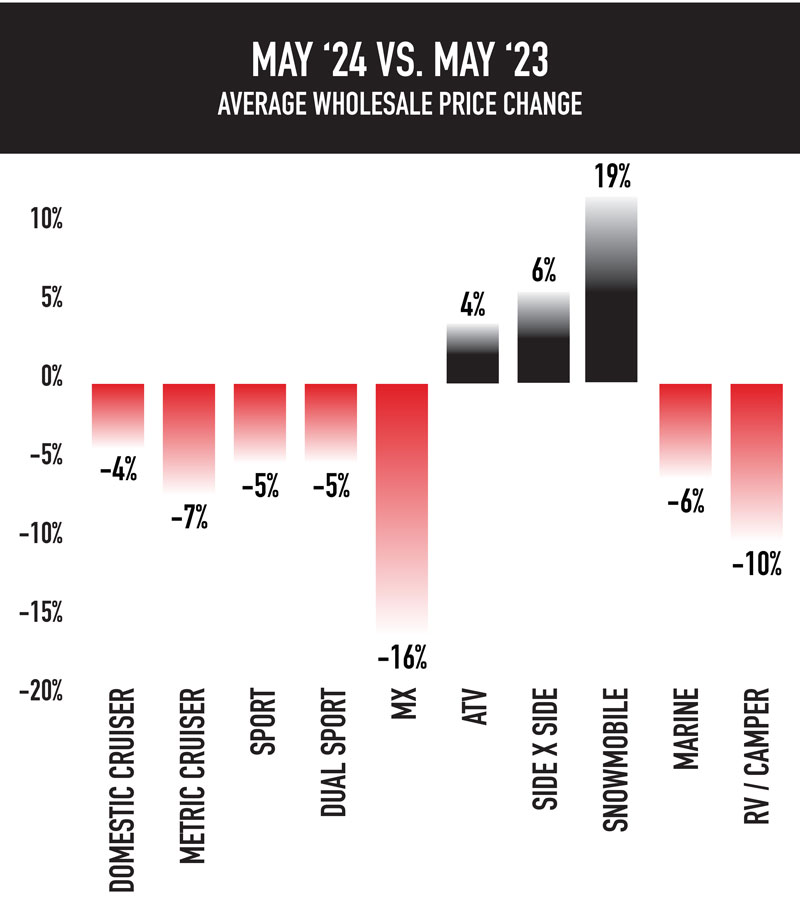

Diving into the category pricing, nearly all On-Highway segments fell versus short-term (prior 90 days) and long-term (year-over-year, YoY) comparables, with the only exception in the Domestic Cruiser category. In contrast, Off-Road AWPs climbed in May with ATV, side-by-side (SxS) and Snow strengthening versus YoY and 90-day comps. Generally speaking, values begin to fall in summer, but the subtle differences between on-highway and off-road trends last month highlight how micro-seasonality within the categories can shift and move in slightly different directions. With the weather heating up across the country and the volume of new inventory continuing to be of concern, dealers must ramp up turn times and move product as swiftly as possible to avoid potential losses. The time to act is now.

Seasonality Trends

As we enter June, dealers, OEMs and lenders are pulling out all the stops to increase consumer interest and spur sales on new products. Promotional activity, incentives and discounts are running high as dealers navigate the rising costs of aging inventory. As we’ve continued to beat the drum of turn times and sales velocity, the trends in auction values continue to support our narrative that the back half of this year will be difficult for dealers who continue to sit on product. Historical trends tell us AWPs will continue to slide month-over-month (MoM) until late Q4, meaning today’s prices will be better than tomorrows. Our advice to dealers regarding moving inventory is to err on the side of speed versus margin. Expect June AWPs to come in 3% to 5% below MoM and YoY values, supporting “normal” seasonal price behavior.